Relative Value Hedge Funds are a category of hedge funds that focus on identifying pricing inefficiencies between related financial instruments rather than betting on the overall direction of markets. By using relative value strategies, these funds aim to generate risk-adjusted returns through market-neutral investing, long/short positions, and hedge fund arbitrage. In an environment where asset prices are increasingly influenced by macro uncertainty, fixed income spreads, and volatility regimes, relative value approaches have gained renewed attention. Explore the detailed article at Tipstrade.org to be more confident when making important trading decisions.

What Are Relative Value Hedge Funds?

Relative Value Hedge Funds are investment funds that seek to profit from price discrepancies between closely related securities. Instead of forecasting whether markets will rise or fall, these funds focus on how one asset is priced relative to another. The core idea is that temporary mispricings occur due to liquidity constraints, market stress, regulatory changes, or investor behavior, and that these mispricings eventually converge toward fair value.

In practice, Relative Value Hedge Funds typically construct long and short positions simultaneously. For example, a fund might go long an undervalued bond while shorting a similar overvalued bond issued by the same entity or within the same sector. Because gains depend on the convergence of prices rather than market direction, these strategies are often described as market neutral.

From an industry perspective, relative value strategies have long been favored by institutional investors for their potential stability. According to research from the CFA Institute, market-neutral strategies tend to exhibit lower correlation to traditional equity markets, particularly during periods of heightened volatility. However, these strategies also rely heavily on leverage and precise risk management, making expertise and discipline critical to long-term success.

The Core Philosophy Behind Relative Value Investing

The philosophy of relative value investing is rooted in the belief that markets are not always perfectly efficient. Even in highly liquid markets, assets with similar risk characteristics can trade at different prices due to temporary imbalances in supply and demand. Relative Value Hedge Funds are designed to exploit these inefficiencies systematically.

Unlike directional strategies, relative value investing does not require a strong view on macroeconomic trends such as GDP growth or inflation. Instead, it focuses on micro-level relationships between securities. For example, two bonds with similar duration, credit quality, and cash flows should theoretically trade at similar yields. When they do not, a relative value opportunity may exist.

Professional managers emphasize discipline over prediction. Relative value strategies often rely on quantitative models, historical relationships, and statistical analysis to identify mispricings. However, experienced practitioners also recognize that models can fail, particularly during market stress. As a result, many funds combine systematic analysis with human oversight to ensure that trades are grounded in economic logic rather than purely mathematical assumptions.

How Relative Value Hedge Funds Work

Long/Short Positioning

At the operational level, Relative Value Hedge Funds rely on long/short positioning to isolate relative price movements. A typical trade involves buying an asset perceived to be undervalued while simultaneously selling a related asset believed to be overvalued. The goal is to capture the spread between the two positions as prices converge.

For instance, in fixed income markets, a fund might identify that a corporate bond is trading at a wider spread than comparable bonds due to temporary liquidity issues. By going long the undervalued bond and shorting a similar benchmark, the fund seeks to profit when spreads normalize. Importantly, the net market exposure is minimized, reducing sensitivity to broad interest rate movements.

This structure allows Relative Value Hedge Funds to focus on relative performance rather than absolute returns. However, execution precision is essential. Small pricing discrepancies often require large position sizes and leverage to generate meaningful returns, increasing operational and financing risks.

Market-Neutral Construction

Market-neutral construction is a defining feature of relative value strategies. The objective is to minimize exposure to systematic risk factors such as market direction, interest rate shifts, or sector-wide movements. Instead, returns are driven primarily by idiosyncratic pricing differences.

Achieving true market neutrality is complex. Correlations between assets can change, particularly during periods of market stress. To address this, Relative Value Hedge Funds continuously monitor portfolio sensitivities, adjusting positions to maintain balance. According to data from the BIS, correlation breakdowns are a major source of drawdowns for relative value strategies, underscoring the importance of dynamic risk management.

Common Relative Value Hedge Fund Strategies

Fixed Income Relative Value

Fixed income relative value is one of the most established and widely used strategies. It focuses on pricing relationships between bonds, yield curves, and interest rate derivatives. Common trades include yield curve steepeners or flatteners, swap spread trades, and bond arbitrage.

During periods of central bank intervention, such as quantitative easing or tightening cycles, distortions in bond markets can create opportunities for relative value funds. For example, differences between government bonds and interest rate swaps may widen beyond historical norms. Experienced managers analyze these dislocations using data from central banks like the Federal Reserve and the European Central Bank.

However, fixed income relative value strategies are highly sensitive to leverage and funding conditions. Liquidity shocks, such as those observed during the 2008 financial crisis, can force rapid deleveraging and lead to losses even when long-term convergence ultimately occurs.

Equity Market Neutral

Equity market neutral strategies seek to exploit relative mispricings between stocks while maintaining minimal exposure to overall market movements. Funds typically construct portfolios that are beta-neutral, meaning gains depend on stock selection rather than market direction.

For example, a fund may go long stocks with strong fundamentals and short stocks with weaker metrics within the same industry. Quantitative models often play a significant role, analyzing factors such as valuation, momentum, and profitability. According to academic research published in the Journal of Finance, factor-based equity market neutral strategies have historically delivered more stable returns than directional equity strategies.

Despite their appeal, equity market neutral funds face challenges related to crowding and factor compression. When many funds pursue similar trades, returns may diminish, highlighting the importance of innovation and data quality.

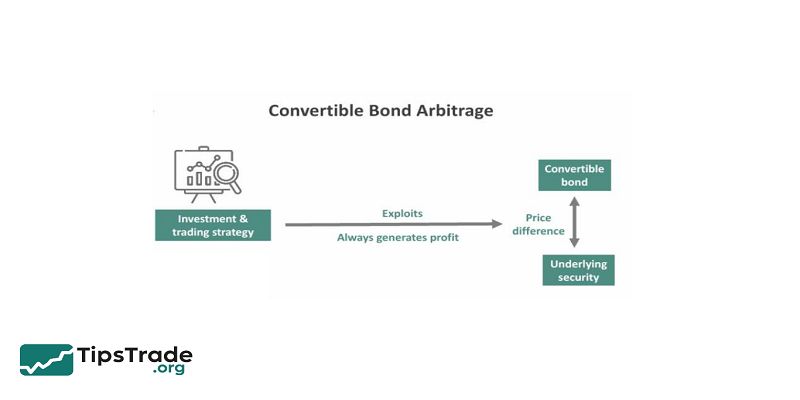

Convertible Bond Arbitrage

Convertible bond arbitrage involves exploiting pricing discrepancies between convertible bonds and their underlying equities. Convertible bonds contain both debt and equity components, making them complex instruments that can be mispriced.

A typical trade involves buying a convertible bond and shorting the underlying stock to isolate the bond’s embedded option value. Relative Value Hedge Funds analyze volatility, credit spreads, and interest rates to determine fair value. According to industry studies, this strategy has historically performed well during periods of moderate volatility but can suffer during sharp market dislocations.

Risk management is particularly important, as convertible bonds can become illiquid during market stress, amplifying losses if positions cannot be adjusted quickly.

Statistical Arbitrage

Statistical arbitrage uses quantitative models to identify short-term pricing anomalies across large sets of securities. These strategies rely on historical relationships and statistical patterns rather than fundamental analysis.

Trades are typically short-term and highly diversified, involving hundreds or thousands of positions. While individual trades may generate small returns, the aggregate portfolio aims to deliver consistent performance. However, statistical arbitrage strategies are vulnerable to regime shifts, where historical patterns break down.

Instruments Used in Relative Value Strategies

Relative Value Hedge Funds operate across a wide range of financial instruments, selected based on liquidity and pricing transparency. Common instruments include:

- Government and corporate bonds

- Equities and equity derivatives

- Interest rate swaps and futures

- Options and structured products

The use of derivatives allows funds to fine-tune exposures and manage risk efficiently. However, derivatives also introduce counterparty and operational risks, requiring robust infrastructure and oversight.

How Relative Value Hedge Funds Generate Returns

Relative Value Hedge Funds generate returns primarily through convergence. When mispriced assets move back toward their historical or theoretical relationships, the spread between long and short positions narrows, producing profits.

Unlike directional strategies, returns are often incremental rather than explosive. According to hedge fund performance studies, relative value strategies tend to exhibit lower volatility and more stable return profiles over time. However, this stability can be disrupted during periods of forced deleveraging or liquidity crises.

Leverage plays a crucial role in amplifying returns. Small pricing discrepancies may only generate meaningful profits when scaled. This reliance on leverage makes funding conditions and risk controls central to performance outcomes.

Risk Management in Relative Value Hedge Funds

Risk management is fundamental to relative value investing. Because strategies often involve leverage and tight spreads, small errors can lead to outsized losses. Professional funds implement multiple layers of risk controls, including position limits, stop-loss thresholds, and scenario analysis.

Liquidity risk is a major concern. During market stress, assets that are normally liquid can become difficult to trade. Historical examples, such as the Long-Term Capital Management crisis, highlight how relative value strategies can fail when correlations spike and liquidity evaporates.

To mitigate these risks, modern Relative Value Hedge Funds emphasize diversification, conservative leverage, and continuous monitoring. Stress testing against extreme but plausible scenarios is now standard practice across the industry.

Advantages and Limitations of Relative Value Hedge Funds

Relative Value Hedge Funds offer several advantages for investors seeking diversification and risk-adjusted returns.

Advantages include:

- Low correlation with traditional equity markets

- Focus on pricing inefficiencies rather than market direction

- Potential for stable, consistent returns

Limitations include:

- Dependence on leverage and funding markets

- Complexity and limited transparency

- Vulnerability during systemic crises

Understanding both sides is essential for informed allocation decisions.

Relative Value vs Other Hedge Fund Strategies

| Strategy | Primary Focus | Market Exposure | Typical Risk |

| Relative Value | Pricing inefficiencies | Low | Medium |

| Global Macro | Economic trends | High | Medium–High |

| Event-Driven | Corporate events | Medium | Medium |

| CTA | Trend-following | Variable | Medium |

Relative value strategies differ from macro and CTA approaches by emphasizing neutrality and convergence rather than directional bets.

Who Should Consider Relative Value Hedge Funds?

Relative Value Hedge Funds are best suited for institutional investors, endowments, and high-net-worth individuals with long investment horizons and tolerance for complexity. These investors often value the diversification benefits and disciplined nature of relative value strategies.

Retail investors typically have limited direct access due to regulatory and structural barriers. However, some alternative funds and ETFs offer simplified exposure to market-neutral concepts inspired by relative value investing.

The Role of Relative Value Hedge Funds in Portfolio Diversification

Within a diversified portfolio, Relative Value Hedge Funds can serve as a stabilizing component. Their low correlation with equities and bonds may help smooth returns over time, particularly during periods of moderate volatility.

However, they should not be viewed as risk-free. Proper sizing and manager selection are critical. Institutional portfolios often allocate a modest percentage to relative value strategies as part of a broader alternatives allocation.

Conclusion

Harnessing Relative Value Hedge Funds empowers investors to thrive in volatile markets. These strategies excel by exploiting price discrepancies across assets, delivering consistent alpha while mitigating downside risks through market-neutral positions. As global uncertainties persist into 2025, savvy portfolios will increasingly rely on relative value approaches for superior risk-adjusted returns. Embrace this sophisticated tool to future-proof your investments today.