Calculating financial ratios is essential for evaluating a company’s financial health and operational efficiency. These ratios use data from financial statements to provide insights into profitability, liquidity, solvency, and market valuation. Mastering how to calculate financial ratios allows investors and analysts to compare companies, identify strengths and weaknesses, and make data-driven decisions. Visit tipstrade.org and check out the article below for further information.

Why Financial Ratios Matter

Financial ratios matter because they translate complex financial statements into meaningful insights. A company’s raw financial data—revenues, expenses, assets, liabilities—cannot tell the full story on its own.

Ratios convert these figures into analytical metrics that support smarter decisions. Analysts use ratios to evaluate profitability, business efficiency, financial risk, and long-term sustainability.

From the perspective of investors and lenders, ratios help determine whether a business is stable enough to fund, whether its debt level is manageable, or whether its earnings justify its valuation.

Business managers, on the other hand, use ratios to track performance trends and benchmark against industry competitors. Real-world experience shows that companies monitoring their ratios quarterly tend to improve financial discipline, according to SBA recommendations.

By understanding financial ratios, readers become better equipped to interpret financial statements, anticipate financial issues early, and evaluate business opportunities more effectively.

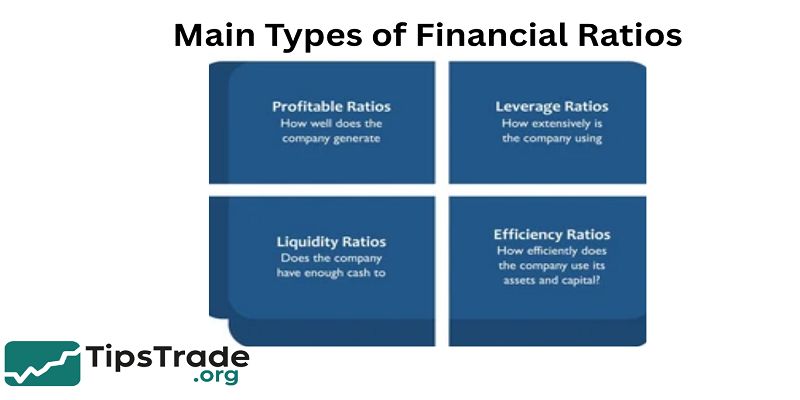

Main Types of Financial Ratios

Financial ratios can be grouped into several categories: liquidity ratios, profitability ratios, leverage (solvency) ratios, efficiency (activity) ratios, and valuation ratios. Each type provides a different insight into the company’s financial condition.

Profitability Ratios

Profitability ratios measure how effectively a company generates profit relative to revenue, assets, or equity.

They help investors determine how well management converts sales and resources into earnings. Common profitability ratios include Gross Profit Margin, Net Profit Margin, Return on Assets (ROA), and Return on Equity (ROE).

For example, ROE shows how much profit a company generates from shareholders’ equity. A consistently high ROE indicates strong managerial efficiency.

Research published by McKinsey & Company highlights that profitability ratios are among the top indicators of long-term business success.

Companies often compare profitability ratios to competitors within the same industry because acceptable margins vary widely.

For instance, grocery retailers typically operate on thin margins, while software companies enjoy high profit margins. Understanding these differences helps users interpret profitability in context.

Liquidity Ratios

Liquidity ratios measure a company’s ability to meet its short-term obligations using available assets.

The two most common liquidity ratios are the Current Ratio and the Quick Ratio. These ratios indicate whether a business has enough working capital to cover immediate liabilities.

For example, a Current Ratio of 2.0 means the firm has twice the current assets needed to pay its short-term debts.

Lenders frequently use liquidity ratios to assess financial stability before approving loans. According to the Federal Reserve’s credit evaluation guidelines, poor liquidity is one of the leading reasons businesses struggle during economic downturns.

Liquidity ratios are essential for small businesses or firms with significant inventory because they help identify cash flow risks early.

A company may appear profitable on paper but still face liquidity problems if its cash is tied up in receivables or unsold inventory.

Leverage (Solvency) Ratios

Leverage ratios evaluate how much debt a company uses to finance its operations. Common examples include Debt-to-Equity Ratio, Debt-to-Assets, and Interest Coverage Ratio.

High leverage may indicate financial risk, while controlled leverage can help maximize returns.

The Debt-to-Equity Ratio measures financial structure. A high ratio suggests the business relies heavily on debt, which may be risky during economic uncertainty.

Meanwhile, the Interest Coverage Ratio measures how easily a company can cover interest expenses using its earnings before interest and taxes (EBIT).

Reports from the International Monetary Fund show that companies with low interest coverage ratios are more vulnerable to rising interest rates.

Therefore, leverage ratios are crucial when assessing risk, especially in industries with volatile earnings such as manufacturing or energy.

Efficiency (Activity) Ratios

Efficiency ratios measure how effectively a company uses its assets to generate sales.

These include Inventory Turnover, Accounts Receivable Turnover, and Total Asset Turnover. Higher efficiency generally means the company manages operations well.

For instance, a high Inventory Turnover Ratio indicates that products are selling quickly, reducing storage costs and risk of obsolescence.

Conversely, low turnover could signal overstocking or weak sales. According to the U.S. Department of Agriculture (USDA), efficiency ratios are especially important for sectors involving perishable goods, where inventory management directly affects profitability.

In service-based businesses, receivable turnover plays a bigger role because it measures how quickly the company collects from customers, which influences cash flow and liquidity.

Valuation Ratios

Valuation ratios help investors determine whether a stock is fairly priced relative to its earnings, book value, or cash flows.

Common ratios include Price-to-Earnings (P/E), Price-to-Book (P/B), and Price-to-Sales (P/S).

For example, a low P/E ratio may indicate undervaluation, while a high P/E suggests strong future growth expectations. Financial research from Morningstar notes that valuation ratios are most meaningful when compared across industry peers because growth rates vary significantly across sectors.

These ratios are essential for stock investors but also useful for private company negotiations and acquisition analysis.

How to Calculate Financial Ratios

Financial ratios are calculated using data from financial statements. Understanding how each ratio works ensures accuracy and prevents misinterpretation.

Step 1: Collect Financial Data

Before calculating ratios, gather data from:

- Income Statement

- Balance Sheet

- Cash Flow Statement

- Notes to Financial Statements

Key items include:

- Total revenue

- Net income

- Operating expenses

- Total assets

- Total liabilities

- Shareholders’ equity

- Current assets & liabilities

- Cash and equivalents

Experienced analysts recommend using audited financial statements from the company’s annual report or 10-K filings. According to the U.S. SEC, relying on unaudited data increases the risk of errors in decision-making.

Once the data is organized, you can begin calculating ratios using standardized formulas.

Step 2: Use Ratio Formulas Correctly

Below is a table of common formulas for quick reference:

| Ratio Type | Formula | Meaning |

| Current Ratio | Current Assets ÷ Current Liabilities | Measures short-term liquidity |

| Quick Ratio | (Current Assets − Inventory) ÷ Current Liabilities | Immediate liquidity strength |

| ROA | Net Income ÷ Total Assets | Profitability of asset usage |

| ROE | Net Income ÷ Shareholders’ Equity | Return for shareholders |

| Gross Margin | (Revenue − COGS) ÷ Revenue | Profit left after production cost |

| Debt-to-Equity | Total Debt ÷ Equity | Leverage level |

| Inventory Turnover | COGS ÷ Average Inventory | How fast inventory moves |

Using consistent formulas ensures clarity when comparing results with competitors or industry benchmarks.

The Corporate Finance Institute recommends always checking whether the formula uses beginning, ending, or average values because different analysts may use different methods.

Step 3: Apply Real-World Examples

Example Company:

- Revenue: $500,000

- Net Income: $50,000

- Current Assets: $120,000

- Current Liabilities: $60,000

- Total Assets: $300,000

- Equity: $150,000

- COGS: $300,000

- Inventory: $50,000

Sample calculations:

- Current Ratio = 120,000 ÷ 60,000 = 2.0

- ROA = 50,000 ÷ 300,000 = 16.7%

- Gross Margin = (500,000 − 300,000) ÷ 500,000 = 40%

Using real numbers helps readers see practical applications. Analysts often use multi-year data to identify trends, which strengthens interpretation and improves forecasting accuracy.

How to Interpret Financial Ratios

Understanding how to read and interpret ratios is just as important as calculating them.

Interpretation Principles

When interpreting ratios, consider:

- Industry benchmarks

- Historical performance

- Economic conditions

- Company size & structure

A ratio is meaningful only when compared to something else. For example, a Current Ratio of 1.5 might be healthy for a tech company but risky for a manufacturing firm with heavy working capital requirements.

Healthline-style interpretation guidelines emphasize that context matters more than raw numbers—financial ratios should guide decision making, not replace judgment.

Trend Analysis

Trend analysis involves comparing ratios across multiple periods. Analysts usually review data for at least the past three years.

Examples:

- Increasing ROE over time → improving profitability

- Declining inventory turnover → potential sales slowdown

- Rising debt levels → increased financial risk

The Federal Reserve reports that companies monitoring trends quarterly are more resilient during economic challenges.

Trend analysis helps identify early warning signs before they appear in traditional financial statements.

Common Mistakes When Calculating Ratios

Relying on Ratios Without Context

A ratio alone cannot determine business health. Companies with high profitability may still face liquidity problems, while firms with strong liquidity may struggle with low margins.

Always compare ratios with industry averages and economic conditions.

Using Only One Ratio for Decisions

Dependence on one metric is dangerous. Lenders look at liquidity, leverage, and efficiency ratios together to determine risk levels. Investors examine profitability, valuation, and growth ratios simultaneously.

The SBA recommends analyzing at least one ratio from each category to obtain a complete view.

Conclusion

Calculating financial ratios enables a clearer understanding of a company’s financial position by translating complex financial data into simple, comparable metrics. When used properly, these ratios support better investment analysis, risk assessment, and strategic planning, making them indispensable tools for financial professionals.